USDA Direct Farm Loans Journey

Working to Improve Customer Experience and Increase Opportunities for America’s Farmers and Producers

Overview

The Customer Experience Center of Excellence (CX CoE) team had the privilege of partnering with the USDA’s Farm Service Agency (FSA) to understand the experience of producers and service center staff in applying for and processing direct farm loan applications.

The CX CoE team applied a farmer-centered and staff-centered design model to tackle this challenge. We conducted interviews and ethnographic observations with over 40 subject matter experts and employees in Washington DC and at six service centers, and almost 40 producers in six states. We also hosted four workshops with stakeholders in Washington, DC to guide the research, update the customer journey map, vet important findings, and develop recommended solutions to improve the customer experience.

Through this research, the CX CoE team built a Journey Map that reflects the experience of producers and loan officers as they move through a typical application.

| Customer Interviews by Location and Date: | |

|---|---|

| Virginia, May 7th–9th, 2018 | Georgia, May 14th–16th, 2018 |

| New York, May 14th–16th, 2018 | Oklahoma, May 14th–16th, 2018 |

| Oregon, June 4th–6th, 2018 | North Dakota, June 11th–13th 2018 |

Findings

At the close of every field research day the researchers gathered to capture and discuss the observations of the day. Some topics and conversations were rich with detail, and lead to the development of a set of customer stories that provide a more detailed look into the lives of these FSA customers.

The customer stories are composites, sometimes bringing in details from several interviews in order to communicate the observations in a more compact and impactful form. Below is a summary of our findings from each perspective. The full stories are available for download. (PDF)

Producer Interview in Oklahoma.

Producer Perspective Findings

“FSA has helped me when nobody else would.”

- I want USDA to understand that this loan application is one small part of my overall journey.

- I need someone who can explain the whole loan process in terms I understand.

- I want to rely on the loan officer to give me good advice and maybe even some business tips for being a successful producer.

- I want individualized help as I fill out the loan application.

- I want to be able to fill out some parts of the application online while still having access to individualized help from my loan officer.

- I want to be able to check online for my loan application status.

Loan Officer Perspective Findings

“I leave the office at the end of the day knowing my support has put another producer on the road to a successful operation.”

- I need reliable technology and connectivity in my office.

- I need a centralized data management system for my customers.

- I want a tool that allows borrowers to see the status of their loan application and then to see their balance and payments on their own so that I don’t spend so much time looking up these details.

- I would benefit from training to help me stay confident through difficult conversations, and to help problem solve with my customers.

- I want my leadership to listen when I come up with ideas about how to help customers more efficiently.

Detailed Findings

1. Producers value in person interactions with Loan Officers.

Observations

- Producers consider a good loan officer as their counselor

- Service center consolidation had downward impact on customer interaction with loan officers

- A poor loan officer creates a negative customer experience

- Training for program technicians is not sufficiently case-based

Recommendations

- Offer offline as well as online solutions to include producers unable or reluctant to use technology

- Consider holistic producer-focused integration across multiple channels

- Technology should augment, not replace, working with staff

- Create a customer-centric organization

Solutions

- Means for producer to share info with loan officer prior to applying

- Increase service center staffing

- Add new service center positions to field basic questions

- Collect, analyze and respond to customer satisfaction data

- Offer new loan officers and program technicians training on handling difficult conversations

2. Obtaining an FSA loan is only one part of a producer’s larger journey.

Observations

- New producers have many other pressing concerns besides obtaining a loan

- Commercial banks often refer producers to FSA

- FPAC offices that share space are more likely to cross-promote services

Recommendations

- Align outreach with the producer’s larger journey

- Make sure the needs of all visitors to farmers.gov are addressed, including needs outside of FPAC

Solutions

- Cross train loan officers and FPAC staff

- Provide an online tool to determine eligibility for FPAC programs

- Consider outreach to commercial lenders to assist in making referrals

- Ensure farmers.gov contains content addressing the broader journey

3. First time borrowers need help understanding the entire loan process.

Observations

- Existing outreach was described as incomplete, filled with jargon, and too hard to find

- Producers were unclear what the eligibility criteria is for direct loans

- Borrowers learned of steps in the process, particularly servicing, as they went through the process instead of upfront

- Borrowers expressed anxiety over not knowing how servicing might work

- The thoroughness of the loan officer is a large factor in how satisfied producers are

- When a loan officer informs the producer in-person what is required, the odds of success are much higher

Recommendations

- Provide detailed information about the entire loan process upfront to first time borrowers

Solutions

- Simplify outreach and make the information more easy to find

- Provide producers a handout of the loan application journey

- Ensure online content describes all stages of the application

- Train loan officers to be more thorough upfront

- Train loan officer to make explicit requests for information early

- Build online eligibility tool

- Recruit experienced producers to mentor new borrowers

- Offer workshops to educate groups of producers

- Post instructional videos online

- Add staff at service centers dedicated to answering basic questions from producers

4. Producers find loan forms challenging.

Observations

- Number of forms and required information is intimidating, but necessary to form a good business plan

- Producers need help from loan officers to complete the forms

- The current checklist can be confusing

- Not every section/form is needed for every producer

- Redundant information is requested

- Existing online PDFs are inadequate

- Repeat borrowers must provide the same information as before

Recommendations

- Reduce complexity of the forms

- Provide clear guidance on exactly what is needed to complete the application

- Provide way to collect form information that supports immediate validation

- Foster reuse of previous form information, rather than require it to be provided for each subsequent application

Solutions

- Simplify forms (e.g. consolidate, less jargon)

- Ensure checklist is clear and concise

- Pre-populate forms with producer information

- Customize loan packet for the producer in person and online (based on input from producer)

- Provide way for producer to access data from prior applications

5. Producers desire self-service to track their loan information.

Observations

- Producers are interesting in viewing their loan information on their own

- A portion of service center staff workload involved responding to inquiries about the loan

- A toll-free number for loan info exists, but few people know about it

- Existing options to obtain loan info are limited to asking staff or waiting for a paper statement

Recommendations

- Provide and promote a means for producers to obtain the loan information themselves

Solutions

- Allow producers to view loan information online

- Promote the existing toll-free number to producers

- Educate service center staff about the toll-free number option

6. Providing the status of a submitted application is complex.

Observations

- The actual processing time for a submitted loan application varies greatly from a few days to several weeks

- If the service center has a backlog of applications to review, a submitted application may sit in queue for some time before review can begin

- The tasks needed to perform a review may vary based on several factors

- The individual review tasks are not always dependent on each other, and may happen in parallel

Recommendations

- Ensure the loan application status reports what is happening with the application similar to how loan staff might respond when asked

Solutions

- Ensure the loan application status reports whether review has started.

- Once the review starts, provide the status of each task involved in the review.

7. Producers are experts in their own information needs.

Observations

- First time borrowers found information (particularly eligibility rules) on the website hard to find and understand

- Producers with existing loans advised new borrowers to do extensive research online before meeting their loan officer

- Producers were unsatisfied with information pertaining to different loan types

Recommendations

- Get input from producers about what content they would like to see

- Write in a voice compatible with how producers think and speak

Solutions

- Conduct user panels and focus groups to gather feedback on content directly from producers

- Follow the guidance of ‘Write for the Web’ to improve comprehension.

- Prior to production, test materials with producers to ensure the information meets their needs

- Ensure the materials can be readily found online or offline

8. Producers doubt their ability to complete an online application successfully.

Observations

- Producers are concerned about submitting a full loan application without input from a loan officer

- Producers and loan officers value the time spent collaborating on a loan application

- Portions of the loan application are straightforward for producers, while others require more assistance

- Some producers are concerned they might lose their work if the Internet cuts out mid-application

Recommendations

- Focus an online application on simple or high-value sections, while enabling collaboration between producers and loan officers

Solutions

- Limit the online application to sections producers can readily complete on their own

- Provide the entire application online, but make only the simple section mandatory

- Allow the producer’s online application to be viewed by the loan officer

- Design the online loan application to be saved frequently

9. Producers find current loan limits constraining and inadequate to cover their needs.

Observations

- Loan limit not enough to support increased cost of operations

- Producers are not aware of the limit

- Producers seeking additional funds must find alternative sources

- Generational producers seek special consideration for higher limit

- Loan officers concerned higher limit would result in fewer loans issued

Recommendations

- Support policy changes to increase the loan limit

- Increase producer awareness of limits

Solutions

- Explain online that limits are statutory

- Work with Congress to increase limits

- Allow producers more flexibility in how loans can be used

10. Producers expect new self-service options to augment, not replace, existing processes.

Observations

- The comfort level of producers with technology varies, but not necessarily due to age or geography

- Producers want to retain their highly valued relationship with loan officers

- Many producers are concerned new technology will replace existing offline processes

- The most favorable self-service options for producers were those that augmented existing services

Recommendations

- Continue to provide traditional channels for support while adding new channels alongside them

Solutions

- Give priority to self-service technology that provides expanded utility to producers beyond traditional channels

- Consider self-service options that continue to involve staff members in the process, while simultaneously reducing their workload

11. Loan officers deal with fragile and limited technology at service centers.

Observations

- Internet and phone systems are not reliable

- Authentication via the Link-Pass card can be difficult

- Inadequate testing of system upgrades historically has resulted in production downtime

- No government supported means for loans officers to communicate directly with producers via text

- Service centers cannot accept cash or credit cards for fees

- Producers have limited channels (i.e. in-person, phone) to conduct transactions

- Service centers are prohibited from working with title companies that do not accept ACH payments

Recommendations

- Highly prioritize the reliability of mission critical systems

Solutions

- Employ phased rollouts

- Modernize critical IT systems

- Inform office ahead of upgrades

- Resolve Link-Pass failures

- Acquire commercial payment system

- Offer alternative payment methods

- Offer live chat help option for producers

- Allow service centers to work with title companies even if they don’t accept ACH for payment

12. Loan data is maintained in a mixture of paper and disjointed IT systems.

Observations

- There are many common activities that require staff to use multiple systems to manually integrate the information.

- The existing workflow is largely paper-based, and creates the need to maintain filing constantly

- Lack of digital workflow means tracking progress of activities manually

- Information is routinely transcribed from paper to a system and then printed out again.

Recommendations

- Prioritize integration of digital tools and workflow

- Ensure adequate funding for building and maintaining IT

Solutions

- Provide an integrated user experience across systems staff commonly use

- Focus on reducing the time required to process payments to reduce the need to track status manually

13. Local service center staff often develop unique, innovative, and producer-centric practices.

Observations

- Service centers self-organize to be efficient

- Service centers without walls separating FPAC staff yields more customer-centric processes and fosters greater staff cohesiveness

- Several offices keep electronic copies of loan paperwork for easy file sharing

- Offices have developed accelerators, such as preparing closing documents as soon as the appraisal is requested

Recommendations

- Embrace new ideas and solutions that are adopted at Service Center locations to isolate root challenges

- Identify, share, and scale locally created solutions that indicate systemic challenges.

Solutions

- Develop forum where service center staff can share their solutions

- Evaluate solutions to identify underlying problems to add to a backlog for resolving

- Have a preference for open workspaces to foster collaboration between agencies

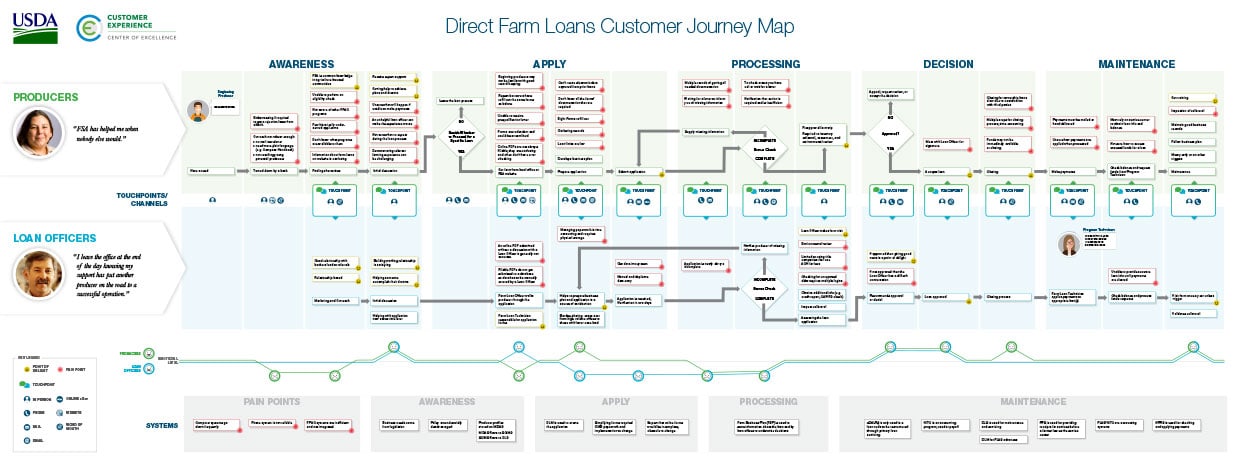

Journey Map

This Direct Farm Loans Customer Journey Map illustrates both the producer experience and the loan officer experience as they move through the process of obtaining and maintaining a farm loan. The map highlights the emotional journey as described by these customers, including their points of pain and delight. In addition, you’ll find the technologies, systems, and touchpoint types used through the process.

Reports

The CX CoE work is guided by user research—structured conversations with a cross-section of farmers, producers, ranchers, and front-line staff. These research reports highlight our findings and recommendations, the methodology we used, and the stories we compiled to explain the typical experience.

Findings & Recommendations Report (2 MB PDF)

Farm Loans Briefing Presentation (13.5 MB PDF)

Want all the specifics of the research we conducted? Download our research methodologies report and the stories report.

What Customers are Saying

FSA helped me when nobody else would.”— Producer

I leave the office at the end of the day knowing my support has put another producer on the road to a successful operation.”— Loan Officer

Farming is a disease. Once you get it, it’s hard to get rid of it.”— Producer

The loan process is a mentorship program to introduce producers to sources of credit.”— Loan Officer

You can’t be a successful farmer without keeping accurate records.”— Producer

Loan limits are way too low for this area. Not even enough to buy seed and fertilizers.”— Loan Officer